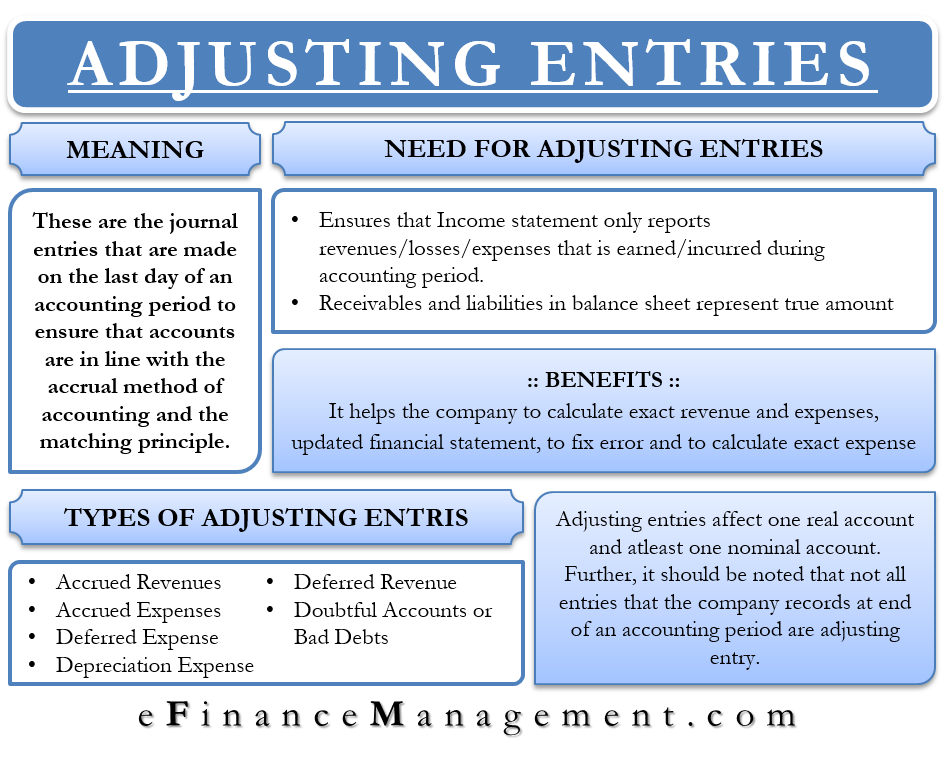

This means the company pays for the insurance but doesn’t actually get the full benefit of the insurance contract until the end of the six-month period. This transaction is recorded as a prepayment until the expenses are incurred. Only expenses that are incurred are recorded, the rest are booked as prepaid expenses. Adjusting entries, also called adjusting journal entries, are journal entries made at the end of a period to correct accounts before the financial statements are prepared. Adjusting entries are most commonly used in accordance with the matching principle to match revenue and expenses in the period in which they occur.

Interested in automating the way you get paid? GoCardless can help

Adjusting entries will play different roles in your life depending on which type of bookkeeping system you have in place. Get free guides, articles, tools and calculators to help you navigate the financial side of your business with ease. The magic happens when our intuitive software and real, human support come together. Book a demo today to see what running your business is like with Bench. Someone on our team will connect you with a financial professional in our network holding the correct designation and expertise. Our writing and editorial staff are a team of experts holding advanced financial designations and have written for most major financial media publications.

Accounting 101: Adjusting Journal Entries

You’ll need to make an adjusting entry showing the revenue in the month that the service was completed. With the Deskera platform, your entire double-entry bookkeeping (including adjusting entries) can be automated in just a few clicks. Every time a sales invoice is issued, the appropriate journal entry is automatically created by the system to the corresponding receivable or sales account. That’s why most companies use cloud accounting software to streamline their adjusting entries and other financial transactions. Manually creating adjusting entries every accounting period can get tedious and time-consuming very fast.

- Depreciation is the allocation of the cost of a long-term asset over its useful life.

- Full-charge bookkeepers and accountants should be able to record them, though, and a CPA can definitely take care of it.

- Office supplies are a good example, as they’re depleted throughout the month, becoming an expense.

- These adjustments are then made in journals and carried over to the account ledgers and accounting worksheet in the next accounting cycle step.

- In December, you record it as prepaid rent expense, debited from an expense account.

Composition of an Adjusting Entry

For example, if a company has an account receivable that is unlikely to be collected, an adjustment entry is made to reduce the value of the asset. Similarly, if a company has a liability that has increased in value, an adjustment entry is made to reflect this change. The primary distinction between cash and accrual accounting is in the timing of when expenses and revenues are recognized. With cash accounting, this occurs only when money is received for goods or services. Accrual accounting instead allows for a lag between payment and product (e.g., with purchases made on credit). Not all journal entries recorded at the end of an accounting period are adjusting entries.

What Is an Adjusting Entry Example?

Adjusting entries are the changes you make to these journal entries you’ve already made at the end of the accounting period. You can adjust your income and expenses to more accurately reflect your financial situation. The point is to make your accounting ledger as accurate as possible without doing any illegal tampering with the numbers. You have your initial trial balance which is the balance after your journal entries are entered. Then after your adjusting entries, you’ll have your adjusted trial balance.

Then, in September, you record the money as cash deposited in your bank account. Adjusting Entries reflect the difference between the income earned on Accrual Basis and that earned on cash basis. This enables us to arrive at the true result of business activities for a given period (e.G., Whether we made profits or suffered losses). Adjusting president kenyatta signs tax laws Entries refer to those transactions which affect our Trading Account (profit and loss account) and capital accounts (balance sheet). Closing entries relate exclusively with the capital side of the balance sheet. The updating/correcting process is performed through journal entries that are made at the end of an accounting year.

For example, if you have an annual loan interest payment due in February and no liability is reflected on the books in January, you’re going to overestimate your available cash. Likewise, if you make an annual business insurance payment and it’s not adjusted, you may believe your overall cost of doing business has increased when it hasn’t. Assets depreciate by some amount every month as soon as it is purchased. This is reflected in an adjusting entry as a debit to the depreciation expense and equipment and credit accumulated depreciation by the same amount.

To record depreciation expense, an accountant would debit an expense account and credit an accumulated depreciation account. To record an accrual, an accountant would debit an expense account and credit a liability account. After preparing all necessary adjusting entries, they are either posted to the relevant ledger accounts or directly added to the unadjusted trial balance to convert it into an adjusted trial balance.